Authors: Robert Nešpůrek, Vojtěch Bartoš, Jaroslav Šuchman

The deadline for the adoption of a Czech whistleblowing act will expire before the year-end – and most likely due to neglect. Nevertheless, the state, regions, municipalities and their subordinate organisations and companies should prepare for the application of the rules of the European Whistleblowing Directive immediately after 17 December 2021.

The EU Whistleblower Protection Directive, commonly known as the Whistleblowing Directive, came into force in autumn 2019. Like any directive, it obliges EU Member States to take such steps at the national level to ensure that the relevant rules jointly agreed by Member States are put into practice.

The Member States are always obliged to fulfil this obligation by a certain date. In the case of the Whistleblowing Directive, that date is 17 December 2021. It is already clear that the Czech Republic will not meet its obligation in time and a Czech law will not be adopted by that date. Breach of this obligation will have one very concrete consequence for public entities in the Czech Republic, which should already be taken into account today, particularly by senior employees of state, regional and municipal organisations, as well as managers of companies backed by the state, regions or municipalities.

After the expiry of the deadline for the adoption of national legislation due to neglect, an individual may directly invoke the application of specific rules contained in the Directive against the State, as if it were a standard Czech law.

Thus, in the case of the Whistleblowing Directive, whistleblowers (employees, workers, contractors and others) will be able to seek some of their rights set out directly in the Directive.

Employers will be obliged to comply with the corresponding obligations under the Directive. These obligations may include, in particular, the obligation to protect the whistleblower, the prohibition of retaliation, the establishment of internal whistleblowing channels or, for example, the obligation to provide information on reports received. These are key rights and obligations arising from the Directive, which are the backbone of the entire whistleblower protection mechanism and the core of the relevant legislation.

It is crucial for everyday practice that the term “state”, i.e. the one against whom the Directive may be directly invoked, should be understood in a broad sense. This is not a new or ad hoc artificial stretching of the concept, but a long, well-established and generally accepted decision-making practice of the Court of Justice of the European Union, which offers little room for doubt.

The Court of Justice understands the term “state” to mean any organisation or body which is subject to the jurisdiction or control of the state or which has special powers beyond the scope of standard rules of private law.

The definition thus includes not only state institutions, such as ministries, independent authorities, state funds and other organisations typically established under or by the operation of law, but also local authorities and organisations established by them. In addition, state-owned or public enterprises and companies owned by the state or local authorities are also subject to state control, and thus undoubtedly fall under the term “state”, as is clear from the CJEU’s decision.

Those responsible for the operation of these bodies, institutions and companies should therefore be aware that whistleblowers will be able to invoke the protection arising directly from the Whistleblowing Directive after 17 December 2021, irrespective of whether or not the implementing Czech act will have been adopted by then. However, whistleblowers will only be able to invoke the provisions of the Directive itself and not the broader concept of protection going beyond the Directive as contained in the current Czech bill.

The immediate consequence of this failure of the Czech legislature will be that whistleblowers will be able to claim in particular internal mechanisms for reporting, will have to be provided with protection if a report is made, and in the event of retaliation against the whistleblower, for example, the whistleblower will be able to claim damages. All this without the Czech legal order laying down more precise rules as to how state institutions are to ensure the above. The provisions of the Directive appear to be quite clear and detailed in these respects.

If you need advice on defining an internal reporting mechanism, please do not hesitate to contact our experts. We know how to deliver a comprehensive solution ranging from a simple, largely standardised solution for a small company, to a tailor-made solution for a group of companies or a public body.

Authors: David Krch, Martina Sumerauerová, Alice Zemánková

Much has already been written in connection with the amendment to the Tax Code as of 1 January 2021, in particular the change in the method of initiating a tax audit by delivering a notice of initiation of a tax audit to a data box. However, the initiation of a tax audit is only one step in many others in a row that the tax administrator usually takes as part of its ‘search activity’. Given that the search activity is usually carried out without the taxpayer’s participation, it is often only by inspecting the file during a visit to the tax authority that the taxpayer learns what the tax administrator was interested in and decided to investigate further.

If the tax administrator comes to the conclusion that it needs to obtain more information in order to correctly determine the tax liability, it may proceed to an on-site investigation. However, an on-site investigation should not serve to comprehensively ascertain or examine taxpayers; this can only be achieved via a tax audit. During the “Covid” times, we also considered the tax administrator’s authority in the context of the massive expansion of work from home, the closure of small sole trader businesses, online children education and the shift of the centre of working life to the homes of a large part of the Czech population.

The rules for conducting on-site investigations are laid down in the Tax Code. However, there is not much knowledge that a situation may occur where an employee or an entrepreneur receives an unannounced visit from the tax authority at home. And since “chances favour only the prepared”, it is advisable to instruct your employees in this context, or to set up internal processes (guidelines) so that the company is immediately informed accordingly and the employee provides only such information that is strictly necessary and relevant to the matter under investigation.

What requirements and what powers of the tax administrator can be encountered during the on-site investigation

And what is an appropriate response to such requests from the tax administrator? The tax administrator’s powers are not unlimited. We may therefore encounter requests made beyond the statutory scope of the on-site investigation. One of them may be an interrogation of the employee present by way of inappropriate questions instead of giving explanations on the matter/fact under investigation.

In addition, employees should be properly instructed and should request the tax administrator to provide proof of their official identity (a service card), request the presence of a manager in charge (such as an internally designated person with a deeper knowledge of the tax audit issues), as well as a request a copy of the on-site investigation report or to ask the tax administrator to enable the recording of the on-site investigation.

Both employees and entrepreneurs using their homes for business activities should be aware of their fundamental rights and obligations in relation to communicating with the tax administrator during an on-site investigation. However, we will be pleased to assist you in setting up the appropriate processes in this area and provide detailed information.

HAVEL & PARTNERS, the largest Czech-Slovak law firm, has promoted Petr Dohnal internally to partner. As an expert in international transactions and distress projects, Petr is a member of the firm’s M&A, private equity / venture capital and insolvency and corporate restructuring practice groups.

“Petr Dohnal has quickly demonstrated his professional and management qualities, which is why he has become a partner 13 months after joining the firm. He will focus on building and managing a robust and stable interdisciplinary M&A team specialising in distressed assets to enable clients to maximise potential opportunities in the post-Covid market,” said the firm’s managing partner Jaroslav Havel.

Petr Dohnal has been actively involved in major transactions across legal and industry sectors and specialises in challenging projects. He is also part of the financing, restructuring and insolvency team, which offers clients comprehensive services aimed at creating the most commercially and risk-efficient solution to their situation in the post-Covid era, including its subsequent implementation.

Petr Dohnal joined HAVEL & PARTNERS last autumn as a major asset having many years of experience in M&A, restructuring and insolvency. Before joining the firm, Petr worked in various legal positions at the PPF Investment Group, where he was involved in a number of projects and transactions on both the sell side and the buy side, particularly in private equity, engineering, transport, construction, IP rights, securities, telecommunications and information technology.

Three new senior associates join HAVEL & PARTNERS to strengthen three of its practice groups. Senior associate Veronika Bočanová joined the family and employment law team. Senior associate Irena Munzarová was engaged by the commercial law team. And the HAVEL & PARTNERS public sector team was boosted by senior associate Dana Prudíková.

Veronika Bočanová is an expert in family and employment law. In family law, she offers comprehensive legal services in relation to marriage and parenting, including setting up childcare conditions, dealing with maintenance obligations, matrimonial property law, managing the estate of minors or legal representation in guardianship proceedings or divorces. In employment law, she has experience in drafting employment documents, defining the content of employment relationships and settling disputes in this context, both from the perspective of the employer and the employee. In both areas mentioned, she has many years of experience from major Czech law firms; she is also a member of the Czech Employment Lawyers Association (CzELA) and the Union of Family Attorneys.

Irena Munzarová specializes in corporate law and all types of domestic and cross-border corporate transformations. She is also heavily involved in acquisitions and sales of companies and real estate law. Prior to joining our law firm, she represented a major residential developer in all of the above practice areas for several years and worked for a major multinational law firm in the corporate and transactions team.

Dana Prudíková focuses on public law, legislation, education, sports, and administrative law. Previously, she was, among others, the Head of the Legislation Department at the Ministry of Justice, and the Deputy Minister for Legislation and International Affairs at the Ministry of Education. She also gained experience with legislative activities at the Legislative Department of the Office of the Chamber of Deputies of the Czech Parliament. She is a member of the Private Law Working Commission of the Legislative Council of the Czech Government. Since the beginning of the year, a total of four dozen lawyers have joined the team of the largest Czech-Slovak law firm; HAVEL & PARTNERS is thus strengthening its personnel across all key legal practice areas in which it has a significant market share to satisfy the high demands and expectations of its clients to the maximum extent possible.

Authors: David Krch, Kristýna Šlehoferová

An amendment to the VAT Act in e-commerce is expected to come into effect in the coming days as part of the ongoing law-making process. The amendment implements the EU Council’s tax package into the Czech system of laws. It also introduces significant changes to imports, cross-border trade within the EU and extends the possibilities for the use of the special one-stop-shops.

Once effective, the amendment will lift the VAT exemption for imports of goods with a value of up to EUR 22. At the same time, to prevent a significant increase in the administrative burden, a new special regime is introduced for low-value imports under which the post office or the carrier, for instance, can assess the VAT on behalf of the recipient of the goods.

In addition, VAT can also be assessed via an extended special one-stop-shop. This change will have a direct impact on the imports of low-value goods especially from e-shops in the US and China, which are very popular in the Czech Republic.

With the amendment, the limits for sending goods in individual members states will be lifted. As for the distance supply of goods, the country of the recipient of the goods is automatically considered the place of supply.

The amendment, however, introduces an exception from this rule under which the country of the supplier can be considered the place of supply. To benefit from this exception, the supplier must be established in a single member state and may not exceed an annual limit of EUR 10,000 throughout the EU in respect to the distance sales of goods and provision of telecommunication services, radio and television broadcasting services and electronic services to the end customer.

Legal fiction will start to apply to electronic platforms: the electronic interface facilitating the sale of goods will be considered to have supplied the goods to the end customer. Therefore, the supply is divided into two transactions:

The shipment is assigned to the supply from the electronic interface to the end customer. The supply of goods from the supplier to the electronic interface is therefore considered the supply of goods without shipment.

These rules only apply to the distance sales of imported goods worth up to EUR 150, i.e. the supply of goods to the end customer from a non-EU member state, and also to the distance sales of goods from a supplier not established in the EU when the goods are already physically present in the EU at the time of sale.

Another major change is the extension of the special one-stop-shop regime to other types of transactions. Until now, the regime has applied to the supplies of telecommunication services, radio and television broadcasting services and electronic services provided to end customers.

The regime will from now on also include low-value imports consisting of the distance sales of imported goods worth up to EUR 150 and the distance sales of goods. For reasons of simplification, electronic interfaces acting as deemed suppliers of goods can also apply this regime to the above transactions.

Two experienced counsels have joined the team of the largest Czech-Slovak law firm HAVEL & PARTNERS. The real estate and construction team has been expanded to include Martin Vlk, who has many years of experience in real estate transactions and builds on his international experience in mergers and acquisitions. Ivan Houfek, an attorney with more than ten years of experience in litigation, M&A and real estate law, has joined the litigation and arbitration advisory group.

“As the leading law firm on the Czech-Slovak market, we are aware that the best law firms are formed by top professionals, so we do not hesitate to invest in the best people on the market. In recent months, we have managed to attract significant assets in senior positions and since the beginning of the year, a total of forty lawyers have joined our team. Thanks to the increase in staff capacity, we are able to meet the high demands and expectations of our clients as much as possible. By acquiring both new senior female and male lawyers, we are strengthening our team across all key areas of law in which we have a significant market share,” said managing partner Jaroslav Havel.

In real estate, Martin Vlk advises clients on sales and divestitures of companies and real estate, the formation of joint ventures, and contractual relationships related to the operation, management and lease of shopping centres, residential, office, industrial and logistics complexes. He also provides legal services in comprehensive commercial contracts and high-risk commercial transactions. Prior to joining HAVEL & PARTNERS, Martin worked with leading international law firms in Prague, London and Bucharest, and also served at the European Court of Human Rights in Strasbourg.

Ivan Houfek specialises in dispute resolution, conducting litigation matters before civil courts and in arbitration proceedings. Ivan has extensive experience in complex litigation and commercial disputes. As a legal advisor, he has been involved in resolving disputes worth billions of Czech crowns. Ivan also focuses on contract law and related disputes, real estate law, mergers and acquisitions, and media law. Prior to joining our law firm, he worked for almost six years at the international law firm Weil, Gotshal & Manges and later managed his own law firm for almost six years. He also gained experience in the appellate panel of the Municipal Court in Prague.

Authors: Kateřina Slavíková, Václav Audes, Sabina Skoumalová

On 14 September 2021, the Chamber of Deputies approved the long-awaited amendment to Act No. 48/1997 Coll., on Public Health Insurance (the “Act”), as returned by the Senate (the “Amendment”). It now awaits signing by the President of the Czech Republic. The Amendment brings a wide range of changes and innovations, such as rules for the entry of innovative drugs and orphan drugs into the reimbursement system, the creation of centres for rare diseases and mental health centres, and the introduction of a definition of a patient organisation.

The most significant change will affect so-called highly innovative medicinal products (“HIMP“) and orphan drugs. The availability of these medicinal products is often very limited and their entry into the system is very complicated due to their specific nature.

For HIMP, which have also received an updated definition, the Amendment should streamline reimbursement approvals, making these medicinal products more accessible for patients.

The Amendment will extend the period for temporary reimbursement (from the original 2 years with the possibility of an extension by another year to the new 3 years with the possibility of an additional 2-year extension).

A legal mechanism will also be set up to allow patients who have been treated with this medicinal product to be treated at the expense of the marketing authorisation holder (the “holder“), pending a switch to comparably effective and safe treatment covered by health insurance. The Senate’s amending bill limited that period to a maximum of 24 months. Patients’ right to receive treatment arises directly from the Act, and it does not therefore require a contract to be concluded between the health insurance company and the holder.

Regarding orphan drugs, the Amendment introduces a completely new system for approving their reimbursement.

Until now, these medicinal products have in practice been funded by health insurance through an extraordinary reimbursement under Section 16 of the Act. At the request of the holder or the health insurance company, the reimbursement will be approved in a special procedure by the State Institute for Drug Control (in Czech Státní ústav pro kontrolu léčiv) (the “SIDC“).

The parties to the proceedings will also be scientific societies and patient organisations, an element that is completely new to the Czech reimbursement system. The law defines so-called soft criteria, which should be used for the assessment of an application for orphan drugs reimbursement (including the importance of the possibility of affecting a disease throughout society). After the SIDC has issued its assessment report, the Ministry of Health (within which a new advisory body is being set up for this purpose) will issue an opinion binding on the SIDC. At the same time, the SIDC will be required to initiate a procedure to review the maximum price of the product within a maximum of 3 years.

For both the HIMP and orphan drugs, the cost of their reimbursement from health insurance must not exceed the amount indicated in the budget impact analysis. If an overrun occurs, the holder will be required to reimburse the amount that exceeded the budget impact analysis figure. It is for this purpose that each health insurance company enters into a contract with the holder containing a provision on how to compensate for costs that would exceed the anticipated level of reimbursement.

On the other hand, thanks to the Senate amendment, the Amendment does not exempt the SIDC from basing the so-called reference basket on foreign prices for actual medicinal products sold on the market and from verifying their actual presence on the market.

The legislative proposal specifically sought to relieve the SIDC of this obligation, in response to judicial practice which criticised the SIDC for taking into account the price of a medicinal product in a given foreign database without examining whether the product was actually marketed in that country. In response to Brexit, the Amendment places Germany among the countries of the so-called reference basket as a replacement for the exiting United Kingdom.

In response to the growing number of mass-produced advanced therapy medicinal products, the reimbursement of these medicinal products will be re-established in the standard administrative procedure after the Amendment enters into force, that is to say, no longer through measures of a general nature.

The Amendment further makes uniform the decision-making process for individual health insurance companies regarding applications for extraordinary reimbursement under Section 16 of the Act and promises to speed up the procedure, reduce administrative burdens for health insurance companies and improve the status of the insured person.

As a matter of fact, clear rules are currently absent for situations where the provision of health services is linked to a prior decision of the medical officer, with a large number of such requests being made annually. These applications relate not only to non-reimbursed health services, but also to medicinal products and medical devices. The Amendment introduces the possibility of providing some health services without prior approval by a health insurance company, for example in the case of urgent care.

An application for reimbursement under Section 16 of the Act will be sent to the health insurance company by

(i) the patient himself/herself or

(ii) the health service provider (in practice, the treating physician will act on behalf of the health service provider).

This reflects current practice, given that it is usually the treating physician who makes the claim for reimbursement.

The Amendment gives the insured person the opportunity to defend himself/herself if the health insurance company rejects his/her claim for reimbursement under Section 16 of the Act. Now, many insured people go to the general courts, but they decide on this matter in a highly ambiguous way. This procedure will now be brought first and foremost to the level of an administrative procedure, and each health insurance company will have to set up an appeal body, a so-called review board.

The Amendment also provides a definition of a patient organisation, meaning “a registered association whose main activity is to help patients and protect their rights and interests”[1]. The patient organization status pertains not only to associations, but also to other legal forms of non-profit organizations, such as an institute or a beneficiary society.

Nurses will be given the authority to prescribe certain medical devices and physicians the authority to prescribe new medicinal products under the Amendment.

The Amendment further increases women’s limit age for paid IVF by one year, from 39 to 40. The age of patients to receive a reimbursed vaccination against meningococcal infections has also been extended. It could also bring more affordable care to patients with severe orthodontic defects, such as clefts, congenital or systemic defects, and extend reimbursement to non-basic dental replacements.

The Amendment also legislated highly specialized health care centres for patients with rare diseases, mental health centres, emergency admissions, and screening centres.

Finally, it is worth mentioning that some other laws will be amended in connection with the Amendment, notably Act No. 592/1992 Coll., on Public Health Insurance Premiums, and Act No. 372/2011 Coll., on Health Services and Conditions for their Provision.

You can read about other events in the Life Sciences world on our blog here.

[1] New provision of Section 113f of Act No. 372/2011 Sb., on Health Services and Conditions for their Provision.

Authors: Ondrej Čurilla, Adéla Havlová

The Court of Justice of the EU published a judgment that may be relevant for the framework agreement awarding practice. There is an established interpretation practice in the Czech Republic, and also established decision-making practice by the Office for the Protection of Competition, according to which a contracting authority is obliged to determine an envisaged value but is not required to publish it or specify it in the procurement documentation (i.e. the contracting authority may keep it as its internal information).

Moreover, the provisions of the Public Procurement Act (PPA) have not implied that when awarding the framework agreement (FA), the contracting authority should specify and notify the suppliers of the maximum quantity or value that it could purchase under the framework agreement.

The Court of Justice of the EU does not agree with this approach, which has also become an established practice in other states.

In case C-23/20, Simonsen & Weel A/S dated 17 June 2021, the CJEU held that the Directive (2014/24/EU on public procurement) had to be interpreted in such a manner that in the contract notice, the contracting authority must specify the envisaged quantity or value as well as the maximum quantity or value of products that are to be supplied under the framework agreement.

Even though the decision largely contradicts the substance of framework agreements (the contracting authorities are unable to define the required quantity in advance, which is why they use FAs to ensure flexibility), it is relevant for the interpretation of Czech regulations and we recommend adhering to it in future procurements.

To avoid facing issues in the future, contracting authorities should, in our opinion, observe the following practical approach:

We recommendspecifying and publishing the envisaged as well maximum unsurmountable value / quantity that can be purchased under the framework agreement. The envisaged value can be set at the upper limit of the estimated scope of supply. The maximum value or quantity may exceed the envisaged value by up to ten or more percent depending on the circumstances. The directive itself lays down 50% of the value of the original contract as the limit for insignificant changes, which could be a justifiable scope.

We recommend specifying the information on the envisaged and maximum value (quantity) in the contract notice but not necessarily laying it down as a binding condition (subsequent) in the framework agreement.

You can reserve an option or an amendment to the FA pursuant to Section 100(3) or Section 100(1) of the PPA, respectively, in the FA. According to the express wording of the PPA, the rules applicable to permitted amendments to contracts under Section 222 of the PPA can also be analogically applied to framework agreements.

Where possible, we recommend adding the information on the envisaged and maximum value of the framework agreement into the procurement documentation. This can be done by means of an explanation of the procurement documentation under Section 98 of the PPA and, in the event of the publication of the public contract in the Journal of Public Contracts, publishing this information also by means of the corrective form F14.

Where the contracting authority specified the envisaged value or another figure in the procurement documentation implying the estimated scope of supply, we recommend not exceeding this limit while performing the FA. These steps can also be recommended where the envisaged value has not been disclosed to the contractors. It will be possible to exceed this limit through possible options, or amendments reserved in the documentation or alterations in the contractual obligation under reasonable application of Section 222 of the PPA.

Should you need a more detailed consultation or legal analysis regarding this matter, please feel free to contact our team at any time. You can also contact us should you have any other questions or to request a legal analysis for your specific situation.

Author: Robert Nešpůrek

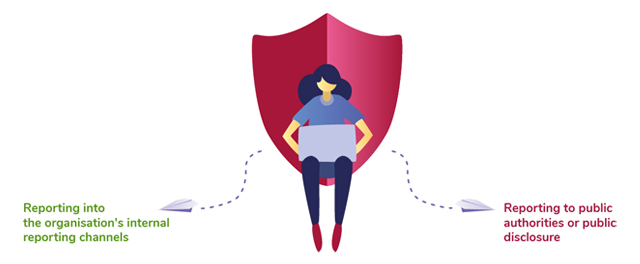

With the implementation deadline for the EU Directive on the protection of persons who report breaches of Union law (17 December 2021) approaching, here is a summary of the current state of the respective national measures in the Czech Republic and Slovakia and an introduction to our own whistleblowing solution: FairWhistle.

There is an implementing bill currently passing through Parliament which will, however, be delayed if not passed into law before the October parliamentary elections. Importantly, the current Czech draft act contains significant deviations from the Directive.

As regards material scope, not only breaches of Union law in the areas prescribed by the Directive are to be reported in the Czech Republic but also:

The draft bill also decreases the threshold of 50 workers prescribed by the Directive for entities in the private sector so that the law should apply to employers with more than 25 workers. In addition, it does not work with gradual adoption as in the Directive but prescribes a single mandatory deadline for all the obligated entities to set up an internal reporting system by 31 March 2022.

In Slovakia, there is already – since March 2019 – a law regulating whistleblowing. The Slovak government has, however, yet to propose a bill adjusting the current whistleblowing law to the Directive. From what we know, the plan is to pass an amendment to the standing law that would bring it in line with the Directive.

The law as it is today requires adjustments to comply with the Directive on several points, including who is to be regarded as a protected whistleblower and who are the other persons concerned, what would count as a retaliatory measure, the various timelines for processing reports and providing follow up to the whistleblower, or the proper setting up of an external whistleblowing channel. It does not look like Slovakia will meet the 17 December 2021 deadline for that amendment to take effect.

Although the Directive brings about a degree of uniformity across the EU block, it is likely that the Czech and Slovak local whistleblowing laws will differ and – as is customary in these latitudes – will also contain specific provisions going over and above the requirements of the Directive. Companies which already have in place whistleblowing schemes will need to reflect that and accommodate these differences.

One such example is the so-called “dedicated person” introduced by the Czech implementing bill. Reports may be channelled only to a dedicated natural person who receives and assesses the validity of a report, manages investigations and follow-ups and communicates with whistleblowers. Such person must be carefully selected and trained and their independence when dealing with reports must be ascertained.

We are following the legislative developments in both the Czech Republic and Slovakia closely and will inform you as it becomes clear when and how the Directive will finally be implemented in these jurisdictions.

In order to help our clients comply with the new regulations, we have designed a comprehensive solution for implementing and managing whistleblowing systems which we call FairWhistle.

We are ready to tailor the entire system (also in view of the fresh ISO 37002 guidance), select the right reporting channels, including a modern web platform from renowned technology partners, prepare all documentation, including appropriate internal communication and training, and then provide support in assessing and investigating reports and act as a “dedicated person”. The objective is to help our clients reduce risk and administrative burden, build ethical organizations and increase their reputation in the marketplace.

With FairWhistle we are capable of providing a tailored and seamless whistleblowing solution to a company of any size or structure. If you are considering how to become compliant with the new rules, do get in touch with us to discuss how best to suit your specific needs.

HAVEL & PARTNERS provided comprehensive legal advice to the credit and loan company, Czechoslovak Business Credit (CSBC), regarding the funding of subsidy projects for BRENS EUROPE, a company whose rail track products facilitate a healthy, fast and quiet transport of the 21st century.

BRENS EUROPE holds an award of the Czech Ministry of Industry and Trade for the “Best product from recycled materials”, and advanced to the finals of E.ON’s Energy Globe 2021 competition.

CSBC helps sole proprietors as well as small and medium-sized enterprises in various situations, such as temporary cashflow-related problems, or long-term investments in upgrades. The company provides bridge financing and assists clients in preparation for bank refinancing.

CSBC is a subsidiary of Czechoslovak Capital Partners, a company dedicated long-term to identifying, implementing and managing investment projects across all areas of business. Since 2012, the group has developed ample experience across the full investment spectrum, having invested over CZK 2.5 billion.

HAVEL & PARTNERS’ specialised M&A team represented the Genesis Capital group, a private equity fund focused on Central Europe, on the sale of a 100% share in the Czech SW development company CN Group, which was taken over by Ciklum, a global company specialised in software development and digital services.

The firm’s partner Václav Audes, senior associate Veronika Filipová and a legal assistant Filip Pavlík provided comprehensive transactional advice to Genesis Capital.

Genesis Capital offers small and medium companies in Central Europe assistance in financing their growth and development. The company has been a long-standing client of HAVEL & PARTNERS, whose specialist not only assisted with the sale of CN Group but also provided legal advice when more than two years ago the fund bought a share in this Czech software company as its first IT acquisition.

“The Genesis Capital Funds acquired CN Group from its founders in 2019 when dealing with succession issues. Over the past 2.5 years, Genesis Capital, together with the management team led by CN Group CEO Michal Širica, has achieved extraordinary multi-fold growth in the company’s revenue and profitability. We are very proud of what has been achieved since our investment in CN Group and wish the entire team continued success,” said Martin Viliš, the Genesis Capital partner responsible for the project.

CN Group is based in Prague and employs 360 digital technology experts. The company provides software engineering, IT consulting and mechanical software design services on more than seven markets.

The company has now been acquired by global IT company Ciklum, which offers software development and digital services to the world’s leading companies and employs more than 3,500 software developers, designers, product managers and data scientists worldwide.

Authors: Robert Nešpůrek, Richard Otevřel

Source: FairWhistle Blog

Correct implementation of a whistleblowing system, as required by the proposed Whistleblower Protection Bill in the Czech Republic, must be understood as part of an organisation’s risk and compliance management.

However, we believe that although it is a regulatory obligation, the introduction of a whistleblowing system can be beneficial to an organisation if handled correctly. The aim should be to create a system that the whistleblower trusts so that the internal communication channel is their first choice. This will give managers or owners a chance to learn about potential problems in the organisation before they start making the headlines. For the whistleblower, the option to make a safe report within the organisation could be a way to remedy a problem they have learned about without causing damage to their employer. Indeed, we should not think of the typical whistleblower as an enemy – in countries where whistleblowing is more common, it is a person who wishes to make things better. If whistleblowing is a well-designed as part of internal processes and is supported by management, such an optimal result can be achieved.

Let’s now take a closer look at what you can gain by implementing a functional whistleblowing hotline:

A model compliance management system, which includes a functional whistleblowing system, is recognised by the methodology of Czech Republic public prosecutor offices as an example of measures that can avert corporate criminal liability. It should be emphasised that the mere set-up of compliance programmes and formal introduction of a whistleblowing system is not enough. Instead, the organisation must be able to demonstrate that it promotes, enforces and adequately monitors these instruments within its personnel structure, and that it is fully prepared to respond to identified deficiencies in the event of a breach.

If the whistleblower has confidence that nothing will happen to them if they make an internal report and that the matter will indeed be investigated, this reduces the likelihood of them going public with their report to the Ministry of Justice or becoming entitled to publish their report in the media or on social media. This prevents major damage to your organisation’s public image and helps protect your trade secrets.

If you identify a problem early, it is more likely to be resolved internally quickly and efficiently before it escalates. This can limit the actual damage (such as the costs of product recall), avoid financial penalties (but sometimes more serious penalties such as a ban on activity), a loss of profit due to damaged reputation, compensation claims and finally legal costs.

Any manager will be pleased if they can manage sensitive matters internally, without the intervention of journalists or even public authorities. If you are the first to know about employee complaints, you will be able to manage such matters within the legal boundaries on your own, i.e. investigate and possibly resolve them without the involvement of external parties. The truth is that once problems are made public, they can live a long life of their own, and unfortunately, often regardless of their veracity.

The implementation of whistleblowing will become a statutory duty and the law will punish inconsistency in implementation with high fines amounting to millions of Czech crowns.

Whistleblowing complements the general structure of an organisation’s compliance and risk management function by giving it an effective tool to discover potential deficiencies and areas for improvement that are commonly identified through lengthy and costly audits.

The introduction of whistleblowing is gradually becoming a standard for companies with a high ethical business culture, which will be increasingly required by investors, shareholders, your business partners (especially international), in public procurement, and also by potential employees.

You might think that you already deal with your internal problems without a whistleblowing hotline. This is certainly a sign of well-functioning relationships within the organisation. But are you sure that you are aware of all cases that you could resolve effectively? Whistleblowing need not be about changing how you solve problems, but it can serve as a useful complement to what you already do in your company. If an opportunity presents itself, why not take advantage of it?